After GameStop, the role of CEO will never be the same

CEOs of tomorrow will be influencers and PR magnates

The short squeeze run on GameStop and other stocks last week was a proverbial throw of the “cat amongst the pigeons”. So much of what was thought to be true about the market is in doubt.

Most people have been reeling from the saga by asking “what does GameStop mean for the future of Wall Street?” and probing into the role of hedge funds and brokerages like Robinhood. That is definitely an interesting discourse, but to be clear is not in scope here. An equally interesting question which is explored here is “what does GameStop mean for the future of companies and CEOs?”

So what is going on right now?

1) Individual investors have been activated by the increasing ease and incentives to trade

Brokerages such as Robinhood, Charles Schwab, Stash, etc are driving significant growth in direct investing. There are three key factors behind this - making it easier, cheaper, and more engaging to invest.

First - they make it easier to invest. Have ever tried to wrap your head around the interface of a legacy broker such as interactive brokers?

Compare this to the slick UI and mobile app experience of Robinhood and you’ll understand the point. Robinhood also introduced features such as fractional share ownership, which makes it possible for your average Joe to own “a share of shares” such as Amazon, now trading at well over $3,200 a share.

Second, they make it cheaper to invest. In 2013, Robinhood launched “zero commission” trading and by 2019, pretty much every brokerage had followed suit. This fact has always been the #1 value proposition emphasized in Robinhood’s marketing, so clearly it resonates with the average consumer. Zero commission trading naturally makes the economics of day-trading (vis-a-vis holding stocks longer term) more feasible.

Third, they raise the incentives to invest. Robinhood and other apps have been accused of “gamifying” investing - “Robinhood reflects how Silicon Valley mastered the art of manufacturing behavioral loops, encouraging an app user to log back in one more time or spend one more minute engaged.” The app incorporates powerful social elements to encourage activity to make it the act of investing more engaging, fun, and addictive.

These factors have all combined to cause a rapid growth in retail investor stock ownership. Robinhood saw a 6x increase in stock ownership on its platform over the 2 years until May 2020.

This, in turn, has had a big impact on the broader stock market. In August 2020, the Wall Street Journal published an article entitled “Individual-Investor Boom Reshapes U.S. Stock Market” which noted that retail investors (as of June 2020) accounted for just under 20% of all market activity, up 4% on 2019.

Other data sources suggest this is under-cooking it and that retail trading could be as high as 25%, and early signs show this share is increasing in 2021.

What is interesting to note is that it doesn’t seem like we are seeing the effects of more people investing than in the past, but rather of people investing more actively. The percentage of people investing in the stock market has actually declined since the early 2000s.

2) The “Reddit effect” amplifies the opportunity for cohesion among retail investors

We have also learnt this week just how big some investor conversational forums have become. In this case, it was the r/wallstreetbets forum on Reddit which, as of today, has exploded to over 7m members (the group started 2021 with 1m members).

It is not just Reddit. There are other thriving forums emerging on Tiktok, Twitter, and other platforms too. Even personal accounts are showing their power to corral retail investors. If you are Elon Musk with 44m followers, you can post a two word tweet in support for the messaging app Signal and cause a 6350% increase in a completely wrong and obscure company that happens to share the same name!

3) The combination of (1) and (2) is creating a new force of market-making - aka the “Robinhood effect”

Combine the growing volume of individual traders and new ease of trading with the simplicity of communication and collaboration and tadaah…

It has been dubbed the “Robinhood effect” - the idea that hordes of investors using the app are socially collaborating and driving irrational stock moves and impulse-buying.

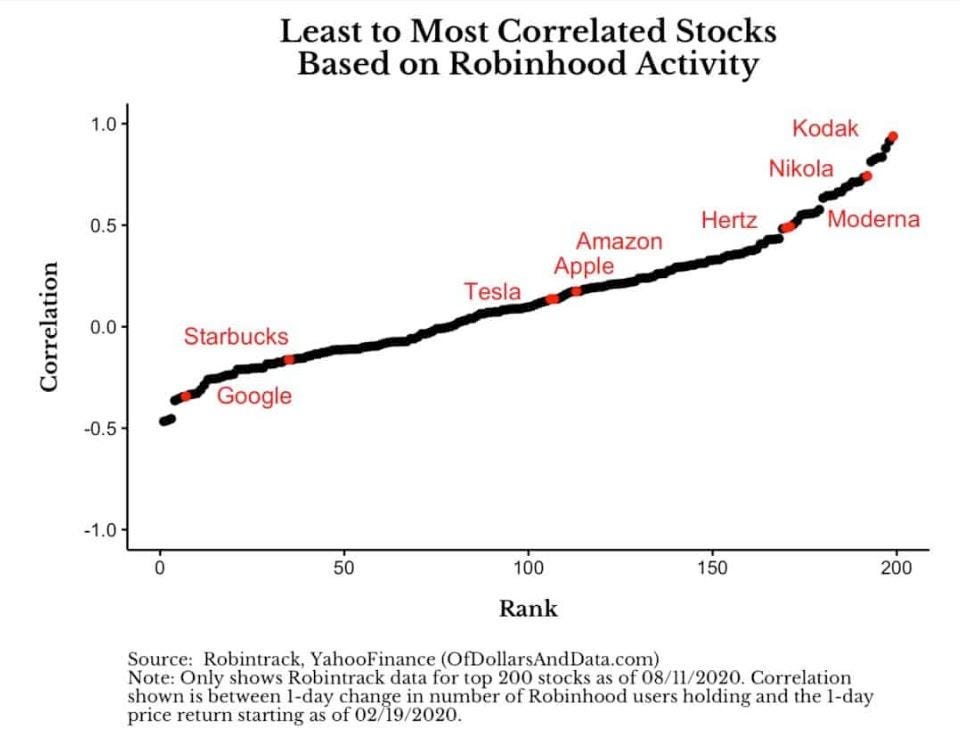

At this stage, such activity appears to be affecting some, but not all, stocks. Nick Maggiulli of Ritholtz Wealth Management ran some analysis and found that there was a reasonably strong correlation between the popularity (the number of people owning the stock) of some small stocks on Robinhood and their share price, suggesting the app’s users may indeed be driving their share prices. Such stocks include Nikola, Moderna, and Kodak.

This correlation was much weaker for larger stocks such as like Alphabet, Tesla, and Apple. One might argue that this is just a matter of time and scale - multiply the number of Robinhood users and r/wallstreetbets members by 20x and then let’s rerun this correlation analysis!

4) This force will only grow and become more pronounced

The “Robinhood effect” is likely to only become more pronounced due to a couple of factors.

First, increasing volume of retail investors and trading. This seems to be increasing not slowing. I saw a pitch a couple of weeks ago from a founder looking to launch the “Robinhood of India”, democratizing access to US equities to the whole of India. The force of the Robinhood effect will be truly amazing if and when it fully globalizes.

Second, growing fluidity of information. r/wallstreetbets has gone from 1m users to over 7m in one month. Such growth in this and other forums will only continue to expand the scope of “group-think”. In the past, you needed scale of capital to move markets (e.g. how George Soros and others came to break the Bank of England). Moving forward, it will be scale of followers.

What does this mean for CEOs?

An argument over the pros and cons or culpability of Robinhood, Reddit, or otherwise is NOT in the scope of this article. The only point to be taken from the above is that the times have changed.

In the past, the market makers were “active” institutional investors who, as an audience, responded most to financial results and stability. CEOs had to speak that language. Jack Welch (former CEO of General Electric) is a good example this generation of traditional CEOs. He ruthlessly focused on building shareholder value through cost-cutting measures, M&A activity, and financial growth. He didn’t maintain much of a public presence and spoke well to institutional investors.

Today, individual investors are emerging as a new and active class of market makers. Beyond the rise in direct investing, no doubt the growth of passive ETFs / index funds is also playing into this. Replacing “active” investing with “passive” automation based on rules such as company size, category, or vertical also reduces the scope of power for institutional investors to “make markets”. And individuals, as an audience, respond not only to financial results but also belief and emotion.

It is also interesting to note that the power of individuals to collaborate and impact (benefit or damage) companies has grown not only in the stock markets, but also in the retail markets. Over the past few years, we have seen a huge rise in consumer activism and boycotting. Boycotts of Ivanka Trump’s clothing line started in 2016 led to the company being shut down in 2018.

So what does this mean to be successful as a CEO? CEOs of tomorrow not only need the skills of CEOs of the past (the ability to steer companies, meet fiduciary obligations, and achieve financial results), but also heightened skills in PR, storytelling, and direct public engagement.

Elon Musk is a good example of this emerging generation of CEOs. Musk has a large cult-like following and is a brilliant story-teller. This is not to say that Musk doesn’t pay attention to the financials like Welch; rather simply that in addition he invests heavily in his public persona and cares more about the opinion of people than the opinion of institutions.

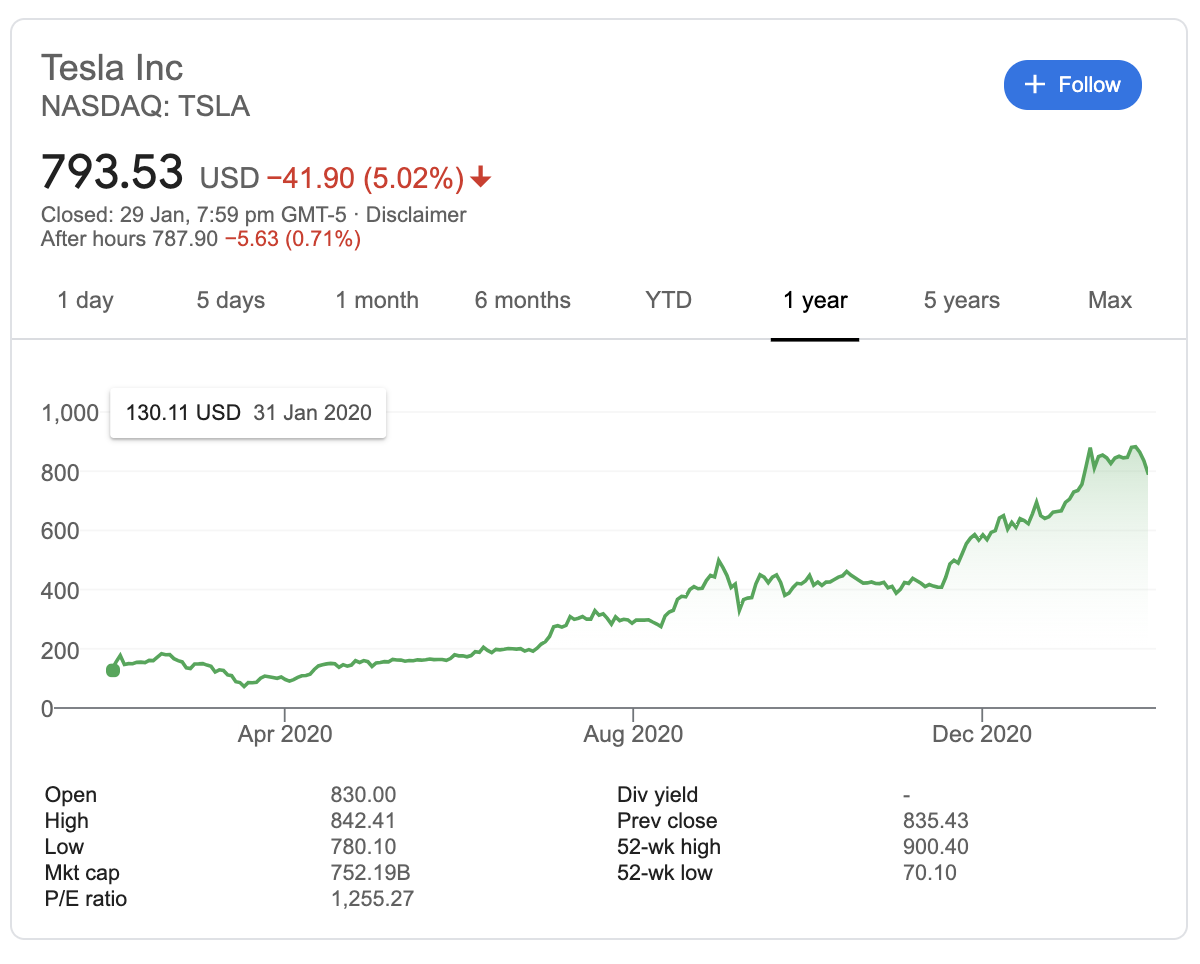

Musk even took the bold step of firing Tesla’s entire PR team last month and has taken over the role himself. He has done many things (posting tweets that breach SEC rules, smoking weed on public radio, etc) that would have spelled certain death for any CEO (and potentially even company) in Jack Welch’s day. Yet Musk and Tesla (up 700% since Jan 2020) has charged on.

In a recent article called “Equity Financing for Influencers“, The Information stated, “The most valuable brands of the future are going to be people rather than companies… You can’t assess Tesla’s $800 billion market capitalization against any sort of realistic view of its financial prospects. The stock isn’t valued as a business but as an Elon Musk trading card.“

This statement may go too far - a good argument for the financial prospects of Tesla can be made. But the point that the most valuable brands of the future will not just orientate around the company but also the people behind them rings true. And naturally, with that growing direct relationship between CEOs and the public comes greater responsibilities, both fiduciary and otherwise.

To be clear - linking this commentary above to the GameStop saga is not to suggest the CEO of GameStop did anything right or wrong. The sole takeaway is that what has unravelled reinforces the power that individual investors now wield and the importance of engaging them.

A shift in private markets too

This shifting role of CEO is can also be seen in private markets too. Gaby Goldberg recently wrote about the rapidly growing trend of founders to “build in public” and how this helps them to build trust and status and attract customers and employees. In raising his recent funding round, Domm Holland of fintech startup Fast talks about how he has been able to use his public presence on Twitter almost exclusively as his source of recruitment. No doubt the emergence of crowd-funding (as with retail funding in the public markets) also expands on the CEO’s need for “public presence”.

It will be interesting to see where this trend leads and the profile of CEOs we will see emerging.

Great article Tom. Completely agree that today's CEOs need to be able to tell the company's story to both retail and institutional investors. Do you think we'll see less CFOs taking on the top jobs and more leaders from product and marketing?